Sarah T.

In this world of immediate gratification, it can be easy to question how long something takes. And it’s not always a concern for the timeline itself as much as it is managing expectations. So, when it comes to saving money on a car loan, it’s only natural to wonder how long does refinancing take.

In this article, we’ll talk about why so many people choose to refinance their car, when you can refinance, and how long the process takes. That way, you’ll know what to expect when you decide it’s time to pursue auto loan refinancing.

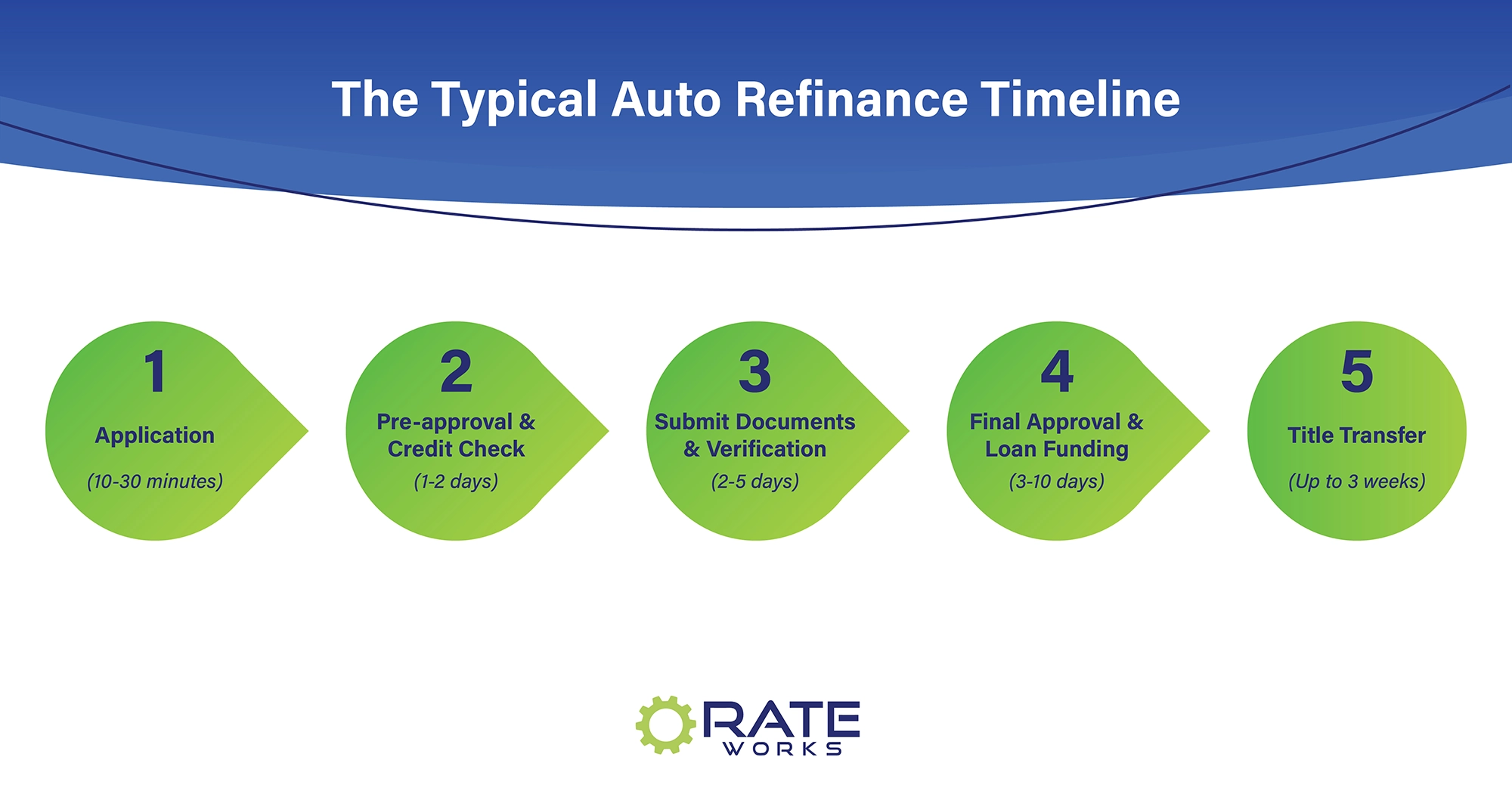

The Typical Auto Refinance Timeline

The first question you might have is, how soon can I refinance my car? Many people refinance their car loans within 30 to 90 days after purchasing their car. Why so soon? Well, oftentimes, dealer financing can be limited, and you can find better rates elsewhere at a later time. So then this begs the question: if you can refinance that quickly, how long does the actual car refinancing process take?

On average, the refinancing process can take anywhere from a few days to several weeks, depending on the lender and how quickly documents are submitted and verified. According to Car and Driver, most auto refinance loans close within about 90 days, though some online lenders may complete approvals in as little as 24 to 72 hours.

Traditional banks and credit unions tend to have longer review periods, especially if additional paperwork or income verification is needed. Online lenders, like Rateworks, often offer a more simplified digital process, allowing you to complete the application, upload documents, and receive approval notifications all from your phone or computer.

Let’s take a look at the overall steps involved in refinancing a car loan, and how long you can expect each of those steps to take.

Step 1: Application (10–30 minutes)

The application process is usually quick and easy, taking as little as 10 to 30 minutes. You’ll need to provide basic details about yourself, your vehicle, and your existing auto loan. This includes your name, address, income, current loan balance, interest rate, and vehicle identification number (VIN). Not sure how to find the VIN on your automobile? You’ll find it stamped on the dashboard, visible through the windshield of your car on the driver’s side.

You will find that many lenders now offer online prequalification. This gives you the opportunity to check and compare potential interest rates without affecting your credit score. This will give you a sense of what kind of refinancing terms you might qualify for before moving forward with a full application.

Step 2: Pre-Approval & Credit Check (1–2 days)

Once your application is submitted, the lender will review your information and run a soft or hard credit inquiry. A soft pull won’t impact your credit score, while a hard pull may cause a temporary dip. During this step, lenders assess your creditworthiness and vehicle details to determine your eligibility and provide estimated loan terms.

You’ll typically receive a pre-approval letter or email outlining your potential new rate, payment, and loan term options. And in some cases, this information may appear directly on your computer screen in the event of an immediate pre-approval (or full approval). That said, understand that a pre-approval doesn’t mean final approval, but it’s a strong indicator that you’re on the right track toward securing a lower rate or better loan terms.

Step 3: Submit Documents & Verification (2–5 days)

After pre-approval, you’ll need to submit supporting documents to verify your identity, income, and vehicle ownership. Providing complete and accurate paperwork helps keep the process on track and prevents delays.

Typical documents include:

- Driver’s license or other photo ID

- Proof of insurance

- Recent pay stubs or income statements

- Vehicle registration

- Loan payoff statement from your current lender

Providing accurate, up-to-date information is important to avoid delays or requests for resubmission. Lenders use these documents to confirm your ability to repay the loan and ensure all vehicle and loan details match up. The faster you provide everything they request, the sooner your refinance application can move toward final approval.

Step 4: Final Approval & Loan Funding (3–10 days)

Once verification is complete, your lender will issue the final approval. At this point, your new lender will typically pay off your old loan directly. You’ll receive confirmation of the payoff, along with details about your new loan terms, due date, and payment method.

Timing can sometimes overlap between the old and new loans, so you may need to make one last payment to your previous lender to prevent late fees. Once the transition is complete, your new loan is officially active, and you’ll begin making payments to your new lender according to your new schedule.

Step 5: Title Transfer (Up to 3 weeks)

The final step involves transferring the vehicle title from your previous lender to your new one. This process is typically handled by the lenders and your state’s Department of Motor Vehicles (DMV). Depending on your state, it can take anywhere from a few days to three weeks.

You don’t need to take any action unless your lender contacts you for additional information. During this time, you can continue driving your car as usual. Once the title transfer is complete, your new lender will officially be listed as the lienholder, and your refinance is fully finalized.

Tips to Speed Up the Auto Refinance Process

Want to help your auto refinance process go as quickly as possible? There are a few things you can do.

- Locate all your documents in advance. This means your last two or three paystubs (your lender will tell you how many you need), a copy of your insurance policy or card, and your most recent car loan statement. Having this all ready to go will make things much easier when it is time for you to upload your documents.

- Take a quick look at your most recent credit report before applying to confirm that everything is accurate and up to date. This can prevent hold-ups during the credit review stage. A free copy of your credit report is available to you once each year through AnnualCreditReport.com.

- While we’re not suggesting that you don’t take the time to compare lenders, choosing a lender like Rateworks that offers online applications and instant pre-approval can help make the process move along a bit faster.

- Respond right away to any lender requests for verification or additional details. The quicker you reply, the sooner your lender can finalize your refinance offer.

- Keep communication open by regularly checking your email or Rateworks account for updates until your new loan is fully approved.

Refinance Your Auto Loan with Rateworks

Refinancing your auto loan doesn’t need to be overly time-consuming or complicated. But, some lenders make things easier than others. If you wanted to keep things simple and quick, consider auto refinancing with Rateworks. All you need to do is request a refinancing quote today to get started. When you work with Rateworks, you’ll never wonder how long does refinancing take, ever again. Why? Because we make it that easy.