Matthew Oliver

There are a few major purchases that we make in life, and buying a car is one of them. And let’s face it. Buying a car is exciting. But, despite the excitement, it also comes with financial pitfalls. Many buyers rush the process, overspend, or lock themselves into loans that strain their budgets for years.

A recent survey of U.S. drivers found that the average American spends 20% of their monthly income on auto loans, fuel, insurance, and maintenance. This is twice the amount most financial experts recommend. In this blog, we’ll break down the 20/4/10 guideline for buying a car, how it works, and why it’s a smarter way to gauge what you can truly afford.

What is the 20/4/10 Guideline?

You may have heard of the 50/30/20 rule for budgeting. This is where 50% of your budget should go toward your needs, 30% toward your wants, and the remaining 20% to your long-term savings. But what is the 20/4/10 guideline, and how can it help you the next time you want to buy a car? We’re glad you asked.

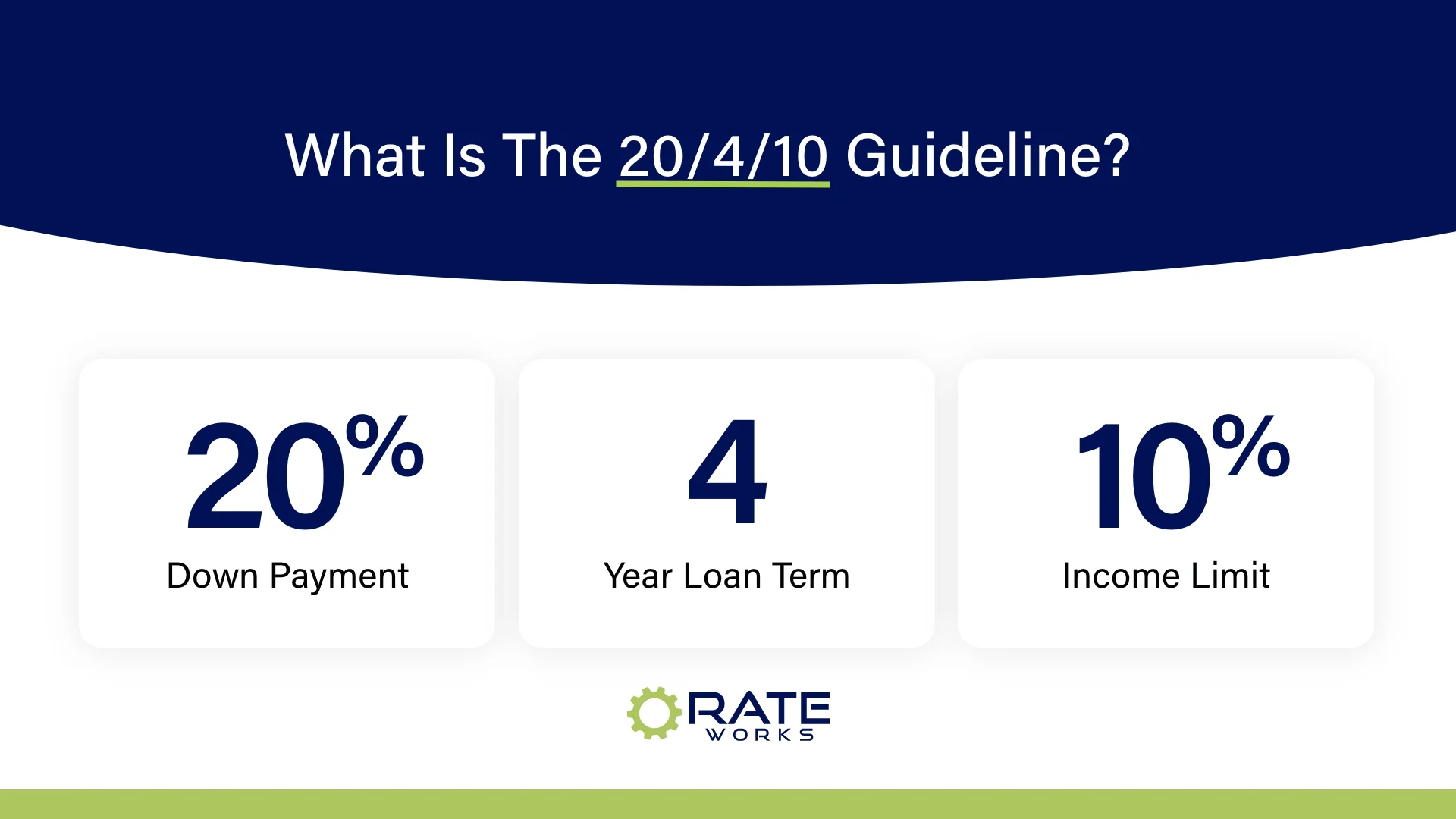

The 20/4/10 guideline is a practical way to keep your vehicle purchase within financial reach and avoid long-term money stress. Here's how each number works:

20% Down Payment

Putting at least 20% down helps you start off with equity in the car. A larger down payment reduces the total amount you borrow, which means smaller monthly payments and less interest over time. It also lowers the risk of going upside down, owing more than your car is worth, especially in the first year, when depreciation is steep.

4-Year Loan Term

A 4-year (or shorter) loan keeps your repayment period tight, reducing the total interest you pay. While longer terms might lower your monthly payments, they often come with higher interest rates and add thousands to your total cost. Plus, shorter terms mean you’ll own the car outright sooner, freeing up cash for other priorities.

10% Income Limit

This part recommends keeping your total monthly vehicle costs, such as your loan payment, insurance, gas, and maintenance, below 10% of your gross monthly income. For example, if you earn $5,000 a month before taxes, all your car-related expenses should stay under $500. This keeps your transportation spending in check and leaves more room in your budget for other needs.

Why Use the 20/4/10 Rule?

Obviously, spending more than you should on a car can have long-term repercussions. Most notably, it means you may not be able to keep up with your payments. If you miss too many, your car could be repossessed, leaving you without reliable transportation to get to work, appointments, or daily errands. And that missed payment? It could hurt your credit score, too.

The 20/4/10 rule helps you stay ahead of these problems by encouraging smart, manageable choices from the start.

Benefits of the 20/4/10 Rule

Following the 20/4/10 rule is about creating financial breathing room. By keeping your car purchase within these guidelines, you’re protecting your budget from unnecessary strain and setting yourself up for long-term stability. Here’s how this simple rule can pay off in a big way.

- Prevents over-borrowing: You limit your loan amount by making a strong down payment.

- Reduces long-term debt: A shorter loan term means you’ll pay less interest overall.

- Keeps your budget balanced: Capping transportation costs helps you cover other essentials without stress.

Why Each Part Matters

Each part of the 20/4/10 rule plays a specific role in keeping your car purchase manageable. Here’s a closer look at why every number in the formula counts.

- 20% Down Payment: Minimizes your loan balance and puts you in a better equity position from day one. This is especially helpful if you need to sell the car sooner than expected.

- 4-Year Loan Term: Shorter terms may mean slightly higher monthly payments, but they save money in the long run. Plus, you'll own the car outright sooner—no payments, no interest.

- 10% Income Limit: Keeps your transportation costs from dominating your monthly budget. This frees up money for savings, emergencies, and day-to-day living.

Let’s share an example. Say you make $60,000 a year—or $5,000 per month before taxes. Based on the 20/4/10 guideline, your total transportation costs shouldn’t exceed $500 per month. That includes your loan payment, insurance, gas, and routine maintenance. If you're considering a $25,000 vehicle, here's how the numbers break down:

- 10% of $5,000 = $500/month max for transportation costs

- 20% down payment on $25,000 = $5,000

- Remaining loan = $20,000

- 4-year loan at 6% interest = About $470/month before adding insurance, fuel, and maintenance

In this case, you’d likely want to explore a slightly less expensive car to stay within the guideline.

Tips for Buying a Car Responsibly

At this point, you’re probably getting the picture: the 20/4/10 guideline is all about helping you stay financially responsible when buying a car. It can be a solid foundation for most buyers, but like any rule of thumb, there are exceptions. Let’s look at when this rule works best, when it might not apply, and additional tips to keep in mind.

When the 20/4/10 Rule Works Best

- You’re buying a reliable daily driver, not a luxury or specialty vehicle.

- You have a predictable monthly income and want to avoid financial stress.

- You’re focused on long-term savings and minimizing interest costs.

- You're financing through traditional lenders and comparing rates in advance.

When You Might Adjust or Skip the Rule

- You're paying in full with cash and have minimal recurring car expenses.

- You're buying a lower-cost used car and only plan to keep it short-term.

- You're in a unique situation (e.g., living in a city with minimal driving needs or working remotely).

- You receive a transportation allowance or car stipend through your employer.

Other Tips for Buying a Car Responsibly

The 20/4/10 rule is a great starting point, but it’s not the only way to stay on track financially. Responsible car buying also means being prepared, asking the right questions, and thinking beyond just the purchase price.

Here are some additional tips to help you make a well-informed decision.

- Check your credit before applying: A stronger credit score can unlock better rates.

- Shop around for financing: Don’t settle for the first loan offer you get. You may be able to negotiate auto refinance rates.

- Consider refinancing options later: If your rate isn’t ideal now, refinancing may be an option down the road.

- Factor in long-term ownership costs: Look beyond just the sticker price. Think fuel economy, insurance, and maintenance.

- Be cautious of extras: Extended warranties, gap insurance, and add-ons can inflate your loan and monthly payment.

Smart Car Buying Starts with a Smart Financial Plan

The 20/4/10 rule offers a clear, simple way to keep your car purchase affordable by focusing on down payment, loan term, and monthly budget. We’ve covered when it works, when to adjust, and how to make smart decisions along the way.

If you already have a loan that feels too expensive, RateWorks offers auto refinancing options that may help lower your monthly costs and reduce interest over time. A better car deal might still be possible. Get a free quote today.

.webp)