Sarah T.

With car prices continuing to rise, it’s no wonder that more and more Americans are turning to auto loans to help foot the bill. And though auto loans are pretty popular, it’s super important to understand how your payments work. After all, when taking out a loan, the chances are that you are paying interest in some form or fashion. This means that not all of your monthly payment goes 100% toward your principal balance.

In this article, we’ll explain what we think you want to know about auto loan amortization. The information we share can help you be better informed when it comes to your auto loans, now and in the future.

What Is Auto Loan Amortization?

We know that amortization is a big word, but it's important to understand the meaning. And thankfully, it’s a pretty simple concept. Auto loan amortization is just the process of paying off your loan in regular, scheduled payments that cover both the principal (what you originally borrowed) and the interest (the cost of borrowing that money).

With an amortized loan, your payment amount stays the same each month, but what that payment covers changes over time. In the beginning, more of your payment goes toward interest and less toward your principal. As time goes on, the balance shifts. By the end of the loan term, you’re putting more money toward the principal and less toward interest. This structure is super common. In fact, most fixed-rate mortgages, auto loans, and personal loans from banks work exactly this way.

What’s an Amortization Schedule?

To make it all make sense, lenders use something called an amortization schedule. This is basically a table or chart that breaks down your loan payment by month, showing you exactly how much of each payment goes toward interest, how much goes toward principal, and how your balance changes over time. It’s a handy tool that gives you a clearer picture of how your loan is progressing.

The key takeaway? Even though your monthly payment might not change, how that payment is applied definitely does. Understanding this can help you plan ahead and maybe even pay off your loan faster if you choose to make extra payments along the way. But before we get ahead of ourselves, let’s go on to discuss how the payments on your vehicle loan are structured.

How Auto Loan Payments are Structured

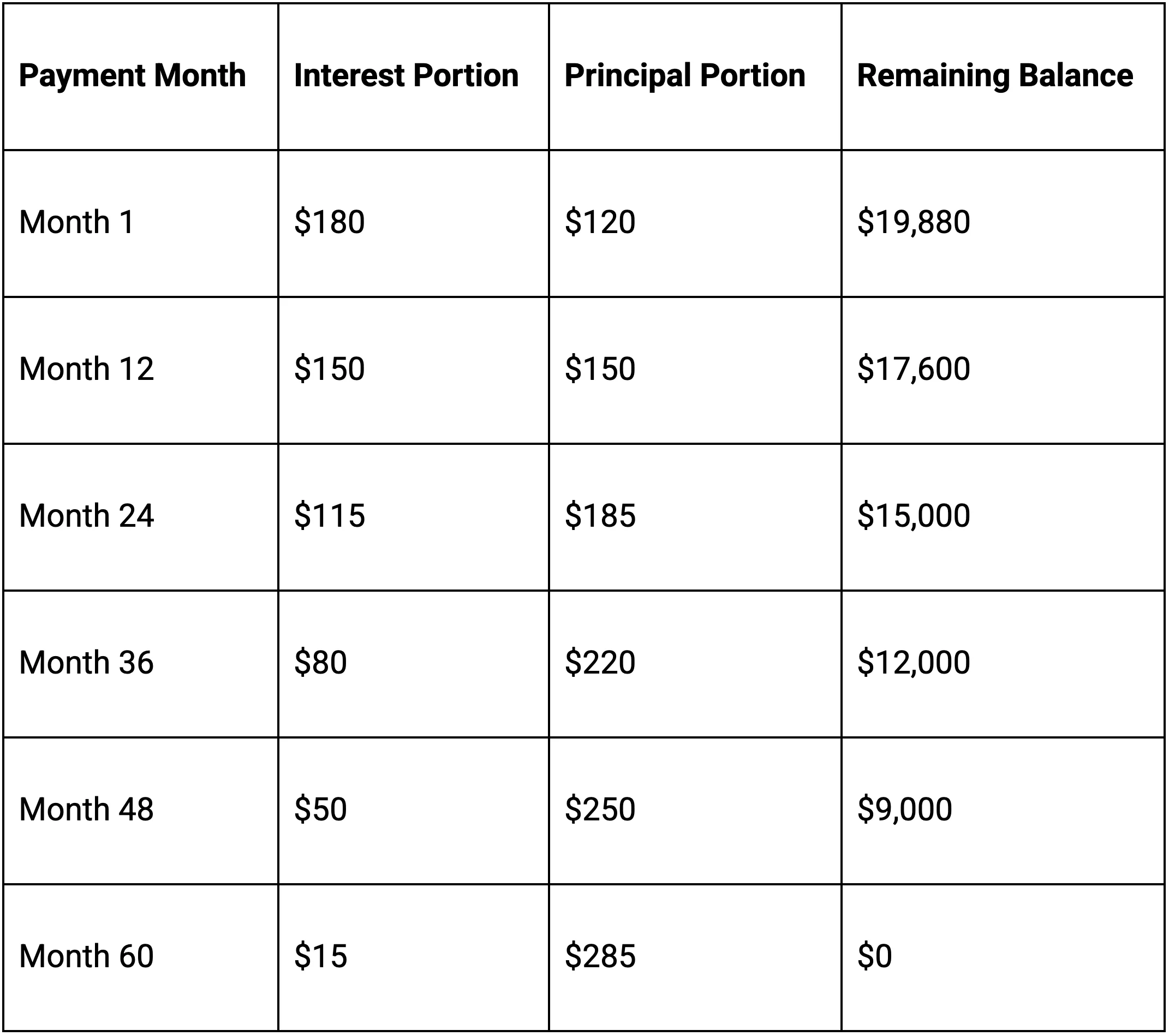

Most vehicle loans come with a set payment schedule for the specified time of the loan. Most auto loans come with payment periods over the course of 24, 36, 48, 60, 72, or 84 months. These payments are divided up so you pay the same amount each month, but what that payment goes toward changes over time.

Here’s how it works: each monthly payment is split into two parts: principal and interest.

- Principal is the actual amount you borrowed to buy your car. This part of your payment helps lower your remaining loan balance.

- Interest is the fee you pay to the lender in exchange for the money they lend you. It’s calculated based on your interest rate and your current loan balance.

In the early months of your loan, a significant portion of your monthly payment is applied toward interest, because your loan balance is still high. Over time, as your balance gets smaller, more of your payment goes toward the principal. This shift is a normal part of loan amortization.

Below is a very simplified example for illustration purposes. For a more accurate depiction of what an amortization schedule looks like, try this car payment calculator.

Why Understanding Amortization Matters

Unless you have some sort of 0% interest promotion for your vehicle, it’s super important to understand how amortization works. And trust us, the days of 0% interest promotions are largely behind us. Today, the average interest rate for a new car loan for someone with a credit score of 750+ is 11.72%. If your credit score is lower, your rate could be even higher.

So why does this all matter? Because the more you understand how your loan works, the more power you have to save money and maybe even pay off your loan faster.

Here’s how understanding amortization can work in your favor.

- You’ll know what you’re really paying for. Knowing how much of your payment is going to interest vs. principal helps you see the true cost of your car over time. This can be eye-opening if you're only focused on the monthly payment and not the long-term total.

- You can make strategic extra payments. If you throw even a little extra money toward the principal early in your loan, you can cut down the interest you’ll pay overall—and even shave months off your loan term.

- You’ll be able to compare loan offers more wisely. Two loans with the same monthly payment can have very different costs depending on the interest rate and length of the loan. Understanding amortization helps you do the math and choose the smarter deal.

An Amortization Example

Let’s say you take out a $20,000 auto loan at 10% interest for 60 months. Your monthly payment would be about $425. Over 5 years, you’ll pay a total of around $25,500. That’s $20,000 in principal and $5,500 in interest.

But let’s say in Year 1, you add an extra $50 each month toward your principal. You’d end up saving about $600 in interest and pay off the loan a few months early. Not bad for a few extra bucks a month.

Common Misunderstandings to Watch For

Understanding how amortization works can help you make smarter decisions, but there are a few common misconceptions that trip people up. Here are some of the most frequent misunderstandings to keep in mind:

- “If my monthly payment is $425, I must be paying $425 off my balance.” Nope. Only part of that payment goes toward your principal—especially in the early months.

- “All loans with the same payment amount cost the same.” Not true. Interest rates and loan lengths affect how much you really pay in the long run.

- “Extra payments don’t really make a difference.” They absolutely can! Especially when made early in the loan term, when interest makes up a bigger chunk of your payment.

- “I don’t need to worry about amortization unless I’m buying a house.” Understanding loan structure helps with any major borrowing, including your car.

Tools for Tracking Your Loan Amortization

Tools for tracking the amortization on your loan are relatively easy to find. And, you might even receive an amortization schedule from your lender as part of your loan paperwork. Earlier, we mentioned using an amortization calculator to get a clearer picture of how your payments break down, but you’ve got another option, too.

You can also try the RateWorks Car Loan Payment Calculator to see how different loan terms, interest rates, and extra payments can affect your total cost and payoff timeline. This tool can help you stay informed and in control.

Looking to Save Money on Your Auto Loan?

Remember when we shared the average interest rate for a new car loan? Yes, it’s pretty high. And this can be a big deterrent to purchasing a new car. But we have some pretty good news for you. In most cases, you can save money by refinancing your loan after the first year (though you can typically refinance your loan as soon as 30 to 60 days after you finance your vehicle).

So, understanding how auto loan amortization works can give you more confidence in managing your car payments and maybe even help you save money along the way. Whether you’re comparing loan offers, making extra payments, or simply planning ahead, a little knowledge goes a long way. And if you're looking for another smart way to lower your car-related costs, consider auto refinancing through RateWorks. Refinancing could help you secure a better rate, reduce your monthly payments, or pay off your loan sooner.